Tony Norfield looks at China-US power relations and examines whether the US can stop China’s rise. This was first published on Tony’s Economics of Imperialism blog.

Can China do much to fight back against the power wielded by the US in the world economy? At first sight, that looks unlikely. China is big, but world trade is conducted in dollars, and the US has economic, political and military influence across the globe. The usual result of a tally of US might is that its position as hegemon is unassailable. But that would overlook how measures of its strength depend upon the world staying in the form that US power has created since 1945. If it doesn’t, then these will not count for as much. As one might expect, China has been responding to US attacks, and the outcome is likely to foment a split in the world economy.

——-

Imagine you wanted to travel from one city to another, but the train company wouldn’t sell you a ticket. Neither would the bus company. Then you were not allowed to buy or hire a car. And anyone who sold you or lent you a bicycle would be fined, or would face imprisonment. With due allowance for analogy, that is similar to what has happened to Cuba, Venezuela, Iran, North Korea and anyone else that the US does not like.

Woe betide you if you are on the wrong side of the US. Then you will find it very difficult to ‘travel’ in the world economy, that is to have any trade or financial dealings. It is not only the sanctions the US imposes; these are also followed to varying degrees by its allies in Europe, Japan and elsewhere. Could the same thing happen to China? It already has, but so far only to a limited extent.

I begin by discussing important dimensions of US power in the world, with a focus on the economic, commercial and financial aspects. I will not deal with the mountains of US weaponry and its means of intimidation with worldwide military bases, although these are significant. The remainder of the article deals with how the rise of China is reshaping the world economy and acting as an alternative focal point to the US.[1] Many countries are paying attention to this, even if the ‘western’ powers do not like it.

Economy & trade in the US-China balance

In the past few years, the Trump-led US administration has stepped up anti-China moves. Even if Trump does not get re-elected in November, this direction of policy is not likely to be reversed by the Democrats. We have seen higher tariffs on China’s exports, attempts to block its companies from receiving any US-made (or designed) products, particularly in the technology sphere, as well as pressure on US allies to exclude Huawei and other important Chinese companies from their domestic markets on supposed ‘security’ grounds.[2]

China’s importance in the world economy means that these exclusion tactics cannot easily be extended. Although the US administration has trumpeted, so to speak, a new objective to cut China out of the supply chains that its big corporations have profitably been using for decades, even the ‘great again’ America must know that this would take many years to achieve.

The US is the world’s biggest economy. With a population of some 328 million people, its GDP in 2019 was $21,439 billion. China has a much bigger population of around 1.4 billion people, but a smaller GDP, estimated at $14,140 billion. China is nevertheless number two in the world, and would be a little bit closer to the US when Hong Kong’s $373bn is added to the mainland China number. Both countries have huge domestic markets of interest to foreign companies, and each has a relatively small volume of international trade when compared to GDP, giving their domestic economies some insulation from the vagaries of the world market. China and the US are the biggest two global exporters and importers of goods, but China is far ahead on exports and the US leads in imports.

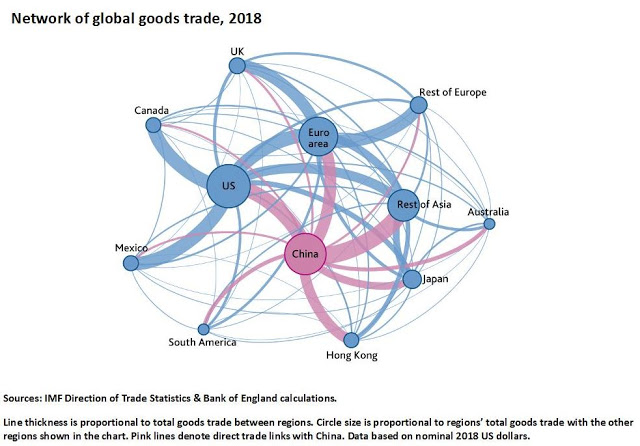

A Bank of England report included an interesting chart of the international trade in goods, showing how China was bigger than the US in trade with Asia and South America, and the US was bigger than China with the rest of North America and with Europe. Unfortunately, Africa was left out of account in this chart, but China’s direct trade with Africa in 2019 was more than three times larger than that of the US.

China’s importance in international goods trade, 2018

The trade pattern shows there are already different relative strengths of the two countries in relation to the rest of the world. Geography goes some way to account for that difference, but one also has to take note of how US companies export from outside the US – including from China – and that many products from China will contain US components. China has a far smaller volume of foreign direct investment and ownership of foreign companies, so its role in world trade is overstated when compared to the US by this simple country-to-country trade picture.

FX power plays

US economic power in the world is shown most easily in the foreign exchange market. This comprises a multitude of transactions, usually across borders, for goods, services and flows of money to buy and sell equities, bonds, commodities, real estate and so forth. Most internationally traded commodities, like oil, copper, wheat and gold, are priced in terms of US dollars, as are many industrial goods like aircraft and chemicals, let alone weapons and illegal drugs. Many countries also have their own currencies directly tied or more loosely linked to the dollar, nearly all central banks hold reserves of US dollar-based securities, and all international companies have dollar bank accounts. As a result, the US dollar is involved in 88% of all exchanges between one currency and another on the international market.[3]

This gives the US government more power than you might think. If a person or a company receives money from selling, or pays money to buy something, then that money has to shift between the bank accounts of the buyer and the seller. When that money happens to be US dollars, the transaction has to go through the US banking system, perhaps indirectly, even if both the buyer and the seller are not located in the US. So, if the US government does not like you, your company, or your country, it can block your ability to use the US banking system.

That would exclude you from the usual channels of world trade and international business transactions. There may be other ways to avoid the dollar entirely and get a transaction done, but these will likely be more costly. And they will also run the risk of the US government using other means of intimidation – for example, when it levies a fine on any bank that processed a deal with you and threatens to stop that bank from operating in the US. This is one way in which the political objectives of the US administration are advanced by its economic power and influence, with no guns needing to be fired.

The centre of gravity

Not only is the US dollar by far the most widely used global currency, the US also has the biggest markets for financial securities, ie for bonds, equities, futures and options contracts.[4] US markets are the centre of gravity for world capitalism. Even though the bulk of transactions in such markets are done within the US itself, the linkages in the global system mean that they filter through quickly into other countries. That is why financial news reports focus most on policy decisions by the US central bank, the Federal Reserve, and the ups and downs of the US stock markets usually have knock on effects elsewhere.

The New York Stock Exchange is the biggest equity market by far, with a capitalisation of nearly $23,000bn at the end of 2019. Nasdaq, also in New York, was the second largest, at nearly $11,000bn capitalisation. Next in line was Japan’s Tokyo Stock Exchange, at a mere $5,700bn, with London at less than $5,000bn.

It is only when China’s three stock exchanges, in Hong Kong, Shanghai and Shenzhen, are taken together that they come anywhere near the US. At the end of 2019, their total market capitalisations amounted to around $10,500bn. However, the Chinese exchanges do have a slightly higher number of corporations listed, some 5,900 compared to a little over 5,300 in the two US markets.[5]

The reason for considering these things is that they are not narrowly financial. For example, a company’s market capitalisation – the total value of its shares – indicates the potential leverage the company has in the broader market. A higher capitalisation means that it can more easily borrow funds from banks, issue bonds itself to get funds, or use its own shares as a means of payment in its takeovers of other companies. Microsoft and Google stand out here, each having done more than 200 takeovers of actual or potential rivals, or of companies that will help them build up a monopolistic position in the market.

It is mostly US companies that figure at the top of the rankings for market capitalisation. In recent years, it has been the Big Tech corporations like Apple, Amazon and Microsoft, each having a number over $1,000bn. China’s Alibaba and Tencent are the only two non-US companies in this top rank, but with valuations of half that of the largest US corporations.

Financial markets magnify US economic power. Not only does the US stock market present its corporations with many billions of market value, that value is also denominated in US dollars, a currency readily acceptable in most of the world. In global terms, it is ‘real money’. Corporations wanting to takeover another will find it easier to do so with US dollars than euros, Japanese yen or sterling, let alone Australian dollars or Norwegian kroner. Apart from its size, liquidity and access to funds, that explains the attraction for companies of listing on the US equity market.

China and the US dollar

The US authorities run access to the dollar, especially the Treasury and the Federal Reserve central bank. So why is it that China, seen by the US as its most dangerous antagonist, has let its economy be dominated by dollars?

First, if China wanted to operate in the world economy, it had little choice 30-40 years ago but to accept the existing structure of world trade and finance. Asia’s economies in particular were, and still are, bound up with the US dollar, through close ties of their currencies and through flows of trade, investment and loans. China has also for a long time followed a policy of keeping its domestic currency relatively stable versus the dollar, even in the wake of the severe crisis that hit emerging markets in the late 1990s. This, along with capital controls, helped keep its economy growing steadily by curbing one source of potential instability.

Second, one method of limiting the impact of possible capital flight is to build up foreign exchange reserves. If foreign investors have assets in China, whether through direct investment in factories, in buying equities or debt securities, then little could be done about the domestic effect on market prices if they sold those assets. But this would not lead to a serious shortage of funds or a collapse of the currency if China’s central bank could sell dollars it already had to counter these flows.

This was an important rationale behind China boosting its official foreign exchange reserves from just $5bn in 1994 to a massive $3.84 trillion by 2014. Some reserves were shifted into state-sponsored purchases of foreign assets (often done using US dollars), some into covering the bad loans of domestic banks, some into offsetting downward pressure on the value of China’s currency in the FX market.

That has still left what may look like an extravagant volume of reserves, totalling $3.1 trillion by end-June 2020. However, such funds have been required on a ‘safety first’ policy.

Consider that China has received a large volume of foreign investment inflow. By the end of 2018, the cumulative amount was $2.8 trillion of direct investment in China, $0.7 trillion in equities and $0.4 trillion in China’s debt securities. Not all of this near-$4 trillion is at risk from capital flight – a chunk of it will also come from Hong Kong – but how much might be vulnerable is unknown. China also has foreign assets of its own that could be sold if necessary: $1.9 trillion in foreign direct investments, and roughly $0.5 trillion in foreign equity and debt securities. This reckoning puts in perspective what otherwise looks like absurdly big foreign exchange reserves.

If anyone thought that a country’s FX reserves had much to do with its international trade in goods and services, the previous figures should put paid to that. Or contrast what happens when you are not as much at the mercy of a potentially destabilising flow of funds. The US has foreign exchange reserves of just $129bn, less than 10% of China’s.

China’s dollar holdings at risk?

Close to half of China’s foreign exchange reserves is held in terms of US dollars,[6] from bank accounts to US Treasury bills and other interest-bearing securities, to gold.[7] The rest is held in other currency denominations, especially the euro. Not just the central bank, but Chinese state agencies, as well as non-state companies and investors, also hold US securities and dollar bank accounts, as well as having dollar liabilities. Could the US government seize China’s dollar assets, or limit China’s access to them?

If seizure of China’s assets looks implausible, consider what has happened to Venezuela’s gold reserves held in the Bank of England’s vaults, or to payments that have long been overdue to Iran! The US could, in principle, also say that the security certificates owned by China – often held in the big US-based custodian banks like Bank of New York Mellon, State Street, JPMorgan Chase, etc – are now invalid pieces of paper, or computer registered items, which belong to an enemy state and now will not be recognised. That would be an extreme measure, also undermining the US ability to attract further funds and investment, so it is unlikely. Such things are usually only done to ‘little’ countries to show them who is boss. But it remains a risk that China’s policy has to manage.

Over recent years, there has been lots of speculation that China could reduce its dollar risk by selling the Treasuries and other US securities that its government and companies own. This would be a foolish thing to do quickly on a large scale, since the prices of the securities could fall in response.[8] Much more importantly, it would also remove the easy access to US dollar funds that China has, and will continue to need, given the dollar-dominated global financial system. What China’s authorities have done instead is to cut back new dollar exposure and quietly offload dollars in the market.

A more comprehensive way of reducing the risk that China faces from US sanctions would be to build another economic, commercial and financial network. Over the past decade, that is exactly what China has been doing.

Your money is no good here

Almost all of the measures used to highlight US economic power depend upon a link to the dollar-based system, for example, the dollar’s domination of the global FX market, the huge capitalisation values of US corporations, and the scale and influence of US financial markets. But what if something shakes the foundations of this power and the global system begins to take on a different form?

Up to now, China’s rise has been evident in production and trade figures. By comparison, its development in the more financial sphere has been limited, but let’s take a look at some of these numbers and what they mean.

The US dollar rules the FX system, with 88% of the $6.6 trillion daily turnover involving the dollar on one side of the transaction. By comparison, even the euro is only at 32%, and China’s currency, the renminbi, is at just 4%.[9] Yet, 38% of the total volume of FX trading is between the dealing banks themselves, and 55% is between banks and other financial institutions, including 9% with hedge funds and other speculators. Only 7% of FX trading is with non-financial firms! What would happen if international financial dealing were less important, especially in US securities? This calls into question the solidity of the dollar’s pre-eminent position in FX markets and in the world at large.

A similar thing applies to the financial power of big US corporations. For example, with a market capitalisation of around $1.6 trillion each in mid-July, it would seem that Amazon, Apple and Microsoft can do pretty much what they like: buy up any budding rival company, run a predatory pricing policy or extend their monopolistic positions further in other ways. But just as a company’s share price can collapse when its prospects no longer look as rosy as before, so can its apparent financial power if it is not able to operate as it wants and finds its markets cut off.

So far these things have not affected the big US corporations very much, although they have faced more constraints than they would like in China’s domestic market. They have not been able to compete well with the domestic champions Alibaba (e-commerce, payments systems, finance), Baidu (a search engine) and Tencent (various operations, from video games to e-commerce, to finance). The boot has instead been on the other foot, as China’s big companies have been edged out of the US and face restrictions in the markets of US allies. Nevertheless, that could change if the US-dominated structure of world markets changes, a development that is well under way.

World in flux

China has prepared itself against US hostility for years. That didn’t take a lot of strategic insight, given the numerous reports to the US Congress complaining about the Chinese ‘threat’ – ie the threat to US hegemony in the world economy, not simply a military calculation. Three international projects have been key: the ‘One Belt One Road’ project launched in 2013, now called the ‘Belt and Road Initiative’ (BRI); the Asian Infrastructure Investment Bank (AIIB), launched by China in 2013-14, and the BRICS Development Bank, now called the New Development Bank (NDB), proposed in 2013-14 and starting up in 2015.

The NDB is headquartered in Shanghai, and initially had enthusiastic support from all its founding members, Brazil, Russia, India, China and South Africa (hence BRICS). They account for 20% of world GDP and 40% of the world’s population, and the NDB looked like it was going to become a big player in development finance. But little activity seems to have taken place in the last couple of years, although there have been important, separate bilateral deals between China and Russia and between China and Iran.[10]

At least partly, this has been due to renewed tensions between India and China, the latest being over their shared border in the north-west of India and India’s ban on the use of 59 Chinese phone apps, including TikTok. The election of Bolsonaro in Brazil, who has criticised China’s investments in the country, is another factor. More importantly, in recent years both India and Brazil have come more under the influence of the US and more anti-China in their policy stance. Bolsonaro has even tried to emulate Trump in this regard, as he has done in his disastrous handling of the coronavirus pandemic.

The Asian Infrastructure Investment Bank (AIIB) has had a more active time, and it now has more than 100 member countries. Not surprisingly, the US did not join, but several of its close allies did, including the UK and Australia. It is a moot point whether the latter were defying the US, or whether they saw joining as a means of keeping an eye on what China was up to – apart from also not wanting to be on the outside to tender for any new contracts. China accounts for nearly 30% of the AIIB’s capital of $100bn, and for 26% of the voting power. Since 2016, this bank has financed a number of power, energy and road projects in the Philippines, Bangladesh, Pakistan, India, Indonesia, Egypt, Turkey and elsewhere.

Belt and Road

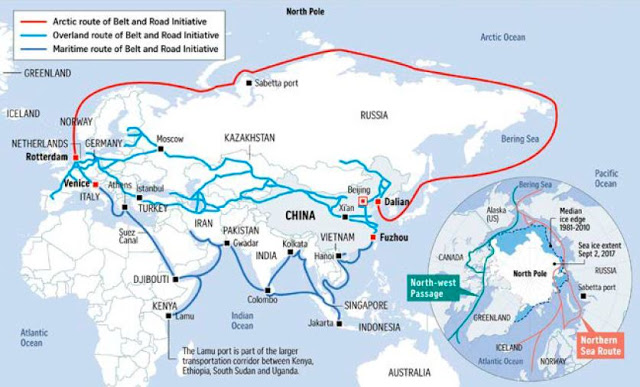

The Belt and Road Initiative is a much more serious plan from China. It has involved more than 130 countries in its projects, and some 30 international organisations. The basic idea is to develop ports, shipping lanes, roads and other infrastructure, including high voltage electricity grids, in a vast enterprise spanning the next 30 years.

The plan’s scope can be seen in the following image, where its routes run all around Asia and Europe and extend into East Africa. It could be considered the beginning of a single market area, but it is nowhere near that yet. Although trade, investment and transit arrangements have been made with other countries along the routes, those countries may often have a cautious approach to dealing with China.

Where the Belts and Roads go

Source: Ewa Oziewicz and Joanna Bednarz, ‘Challenges and opportunities of the Maritime Silk Road initiative’, October 2019

Europe, in particular, is wary. Not only because the relevant powers are not used to a ‘developing country’ having so much leverage, but also because they have been within the US sphere of influence. Yet they are growing worried about that, given Trump’s unilateralist ‘America First’ approach that has also targeted their industries for extra import tariffs, and their fear of the role of US Big Tech corporations. While they have joined in some moves to curb Chinese companies, this has been only to a limited extent so far.

As the political leaders of the European Union, Germany and France will have to make up their minds which way to jump. Yet that process will take some time to play out. For the time being, they are working on trying to cohere the EU itself as the UK leaves, and they hope that the EU can play the role of being an independent actor in the world economy.

The UK, ex-EU and ex-much else, is far more tied to the US. It has legions of political figures and economic interests integrated with the Anglosphere global set up, from the UN Security Council, to military cooperation, to the ‘Five Eyes’ spy network, to the rules applied to finance and trade at the BIS, IMF and WTO, to deluded hopes for a special Brexity relationship with the US in the future. These things will weigh on British decision-making, and the resulting disarray in and confusion of an arrogant imperial power should be amusing to observe.

The Belt and Road project is very important for China, and opponents can easily cast it as simply a tool with which China secures safe routes for its exports and imports. It has also had negative media coverage because of signs of unequal deals, projects that have led to large indebtedness for the country concerned, or projects in which a commercial port is claimed to be a cover for a potential Chinese naval base (as in Sri Lanka), or potential Chinese takeover and ownership when the debt cannot be repaid or serviced.

Evidence I have seen points to a more positive assessment. At least some of the problems with projects have been due to local corruption as much as to any Chinese misdemeanour. It is also worth noting that China’s infrastructure development plans often include building schools and hospitals as well as improving energy supply. The BRI should act to integrate more isolated areas into the world economy, greatly speed up logistics, travel and transport, and help these regions grow. It is not in China’s long-term interests that cooperating regions and countries become mere servicing wastelands.

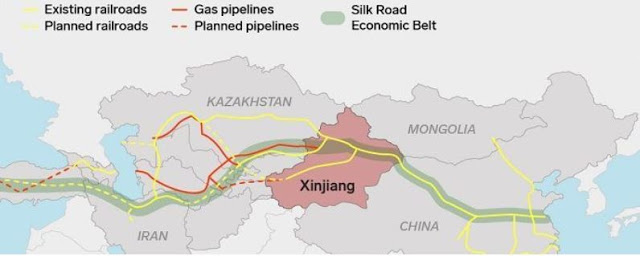

The Xinjian crossing

The BRI’s routes traverse areas in which US imperialism has long sought to gain influence, many of which were formerly inside the USSR – including Kazakhstan, Uzbekistan, Turkmenistan and Georgia – and also Iran and Russia itself. One area along the route that has been prominent in the news media recently is Xinjiang in north western China.

Xinjiang, or to give it the official title, the Xinjiang Uyghur Autonomous Region, is home to around 25 million people, of which 45% are of the Uyghur ethnic group, and many of these are Muslim. It is China’s largest natural gas producing region, and has been the locus for many attacks by Islamic separatists, especially since the 1990s. Plausible reports claim that this was a ‘blowback’ from previous Chinese arming and training of Islamic guerrillas to fight Russia in Afghanistan in the 1980s. China, along with Pakistan, Saudi Arabia and others, cooperated with the US CIA in this period, and trouble brewed for China in this region when the guerrillas came home.

The US, UK and other western powers have a long history of using Islamic militants to do their dirty work of political disruption and destabilisation, even though it often comes back to bite them. Just think of Osama Bin Laden and the support the US also gave his organisation to attack the Russians in Afghanistan. Or the British support for Islamic militants in Egypt against Nasser and in Libya against Gaddafi.[11] It is therefore no surprise that the US has been heavily involved in promoting Uyghur separatists, and that western news media have been full of stories about Chinese ‘concentration camps’ and brainwashing centres for Uyghurs.

BRI & the Xinjiang Region

Source: World Affairs blog, see footnote 12.

It would take too long and be too off topic to cover this in more detail, but my basic view is this. China has not been kind to separatist forces in Xinjiang and may well have clamped down on them harshly. It has also encouraged Han Chinese to move into Xinjiang. But there is no evidence of actual or cultural ‘genocide’ of Uyghurs and the region has even had some autonomy from strict regulations imposed elsewhere in the country, for example, on population and family policy. The western media view of all this is readily available; for an informed alternative view, I give some sources in a footnote.[12] Surely, anyone with any sense would see that there could not possibly be a ‘Save the Muslims’ motive behind the western propaganda about Xinjiang.

Hong Kong less important for China now

As the US anxiety and near-hysteria about China has grown, another opportunity has arisen for mischief – in Hong Kong, especially since early 2019. There have been widespread protests in this ‘special administrative region’ of China against the introduction of laws that would increase mainland China’s authority and potentially suppress dissent and opposition to government policy. Although led principally by students, the protests clearly had support from a large section of the population of Hong Kong.

Beijing was obviously none too pleased with this, and its paranoia alarm bells rang loudly when some demonstrators carried US flags and called for the US to impose sanctions on Hong Kong to force China to drop its proposals. (The US has now done it.) With the CIA-backed National Endowment for Democracy supporting the protests and with Joshua Wong, one of the leading students, cosying up to arch reactionary and regime-change interventionist, US Senator Marco Rubio, the stage was set for a Chinese clampdown.

China’s political system is authoritarian, but one should not fall for the hypocrisy of western powers lamenting the threat to a tradition of democracy in Hong Kong. Prior to UK talks with China in 1984 about the handover of Hong Kong in 1997, there was no sign of democracy, but instead an oligarchic Legislative Council, an advisory body to the British Governor. Full elections to this Council only began in 1995. So ‘democracy’ began to be introduced only just before Britain was going to lose its colony after 99 years.

What will be China’s policy towards Hong Kong now? To answer this question, it is worth noting the role it has played in relation to China.

When it was a British colony, Hong Kong specialised as an entrepot centre in Asia, with a large port operation and a big financial sector. As China grew as a global production base, particularly from the 1980s, Hong Kong also thrived as the ‘western’ gateway into China, with booming cross-border deals. In turn, China used Hong Kong to gain experience of international markets, from how best to run a port to how to manage banking and finance.

Hong Kong is now less important for China than it might seem. Its GDP is less than 3% of mainland China’s, and its 7.5 million people could be seen as barely a rounding error compared to China’s total. It is nevertheless politically inconceivable that China would allow Hong Kong to become fully ‘independent’ or to secede. In the event of continued protests about rule by mainland China, a much more likely policy would be to slowly run down the remaining economic reliance China has on Hong Kong. This is no doubt on the minds of some Hong Kong residents, not all of whom are anti-Beijing.

Hong Kong’s population has significantly higher living standards than the average in mainland China, and US dollar millionaires make up a surprising 7% of the population. Such factors will have influenced the protest movement in Hong Kong, and there have also been many signs of locals resenting mainlanders. Some of the latter have been attacked for supposedly being Beijing loyalists; others have faced opposition from locals who felt their presence was driving up prices and rents. I think that fear of an economic ‘levelling down’ is at least as significant a factor in the protests as any call for democratic rights.

Top 10 World Container Ports, Volume in millions of TEU *

| Rank | Port | 2018 | 2017 | 2016 |

| 1 | Shanghai, China | 42.01 | 40.23 | 37.13 |

| 2 | Singapore | 36.60 | 33.67 | 30.90 |

| 3 | Shenzhen, China | 27.74 | 25.21 | 23.97 |

| 4 | Ningbo-Zhoushan, China | 26.35 | 24.61 | 21.60 |

| 5 | Guangzhou Harbor, China | 21.87 | 20.37 | 18.85 |

| 6 | Busan, South Korea | 21.66 | 20.49 | 19.85 |

| 7 | Hong Kong, S.A.R, China | 19.60 | 20.76 | 19.81 |

| 8 | Qingdao, China | 18.26 | 18.30 | 18.01 |

| 9 | Tianjin, China | 16.00 | 15.07 | 14.49 |

| 10 | Jebel Ali, Dubai, United Arab Emirates | 14.95 | 15.37 | 15.73 |

Source: Worldshipping.org. Note *: The data represent total port throughput, including empty containers. A TEU is a ‘Twenty-foot Equivalent Unit’. The dimensions of one TEU are equal to a standard 20-foot shipping container.

One way of judging the ability of China to sideline Hong Kong, if it wants to, is by looking at its importance as a port. A list of the top world container ports – containers are critical in the trade of goods – has mainland China with six in the top 10. Hong Kong’s port is large, but is ranked number seven and is only roughly half the size of Shanghai’s at number one. Shenzhen, at number three and also bigger than Hong Kong, is only around 15 kilometres from Hong Kong (although a bit further to travel by sea!).

Out of control

Rivalries in the world economy can bring unexpected results, especially when a former underdog can now pro-actively resist. The world order is no longer entirely one where, as Bob Dylan put it, ‘You’re dancing with whom they tell you to, or you don’t dance at all’. How far China is able to build stable alliances for an economic area that limits US interference, and whether it too becomes oppressive, remain to be seen. But in the meantime it has offered many countries an alternative to the rich country model of development, one that has left poor countries poor.

Prospects for the Anglosphere powers are not good. Political idiocy born of generations of arrogance now adds to their difficulties in navigating a world that is changing increasingly outside their control. Examples of their recent responses to Chinese technology sum up their problem. China’s Huawei produces very good, and cheaper, 4G and 5G products, including infrastructure and smartphones, and ByteDance also has a popular media app, TikTok. Instead of saying, ‘we have something even better’, the US and others respond by claiming, with no evidence, that they pose a security risk and that Chinese products should be rejected.

By contrast, Germany, the most productivist of the European powers, has shown more enthusiasm for China-led developments than others. The Belt and Road Initiative already has an important outlet in Duisburg, the world’s largest inland port, where it is the first European stop for 80% of Chinese trains:

“Every week, around 30 Chinese trains arrive at a vast terminal in Duisburg’s inland port, their containers either stuffed with clothes, toys and hi-tech electronics from Chongqing, Wuhan or Yiwu, or carrying German cars, Scottish whisky, French wine and textiles from Milan heading the other way.”[13]

Duisberg’s main problem seems to be that ‘for every two full containers arriving in Europe from China, only one heads back the other way, and the port only earns a fifth of the fee from empty containers that have to be sent back to China’.

At the other end of the line, another German company, BMW, has praised China’s technical know how:

“The auto industry is undergoing a major transformation driven by technological development. In the midst of industrial upgrading and transformation, we need to keep an open mind and to collaborate with outstanding Chinese innovation powerhouses.”[14]

To say the least, these things suggest that China’s growing importance in the world economy will be difficult for the US to curb.

Tony Norfield, 14 July 2020

[1] Other articles on this blog have also analysed US-China relationships, including one from May 2011, looking at the growing strategic tensions, one in April 2019 on the economic and technology competition and another in September 2019 on the relative positions of the major powers. I cover the coronavirus pandemic here.

[2] The US makes much of the links, actual or alleged, between top Chinese companies and the Chinese Communist Party, the military, etc. For reasons that only an evil commie would speculate upon, it seems to forget that Amazon, Google and myriads of other US corporations, not just the arms producers, derive a lot of funding and regular contracts from the US government, the CIA and the Pentagon.

[3] See the article FX & Imperialism on this blog, 7 October 2019, for further details of the role of the US dollar compared to other currencies.

[4] Although London is the biggest market for dealing in foreign currency and for interest rate swaps.

[5] Both totals will include some companies listed on more than one exchange. Nearly 20% of companies on the two US exchanges are foreign companies; there is no comparable figure available for China, but it is likely very much lower.

[6] China does not usually disclose the currency composition of its FX reserves, but China’s SAFE has reported that the dollar component of reserves fell from 79% in 1995 to 58% in 2014. It will have fallen further since 2014, and is likely now a little under 50%. The absolute volume of dollars held will have risen up to 2014, given the big rise in total reserves, but will have likely fallen since.

[7] Over the past 10-15 years, China’s central bank has boosted its gold reserves from 600 tonnes to 1,917 tonnes. At $1,700 per troy ounce, this amounts to ‘only’ $106.5bn and a little over 3% of the reserves total at present.

[8] I say prices ‘could’ rather than ‘would’ fall because of the huge size of the US interest-bearing securities market, especially for shorter-term US Treasuries and agencies, which would limit the response to any selling by China.

[9] FX deals involve two currencies, so adding the shares of all currencies traded would give 200%, not 100%.

[10] Going against US sanctions, in July 2020, China and Iran have drafted a deal covering trade, investment and military cooperation. See New York Times, ‘Defying U.S., China and Iran Near Trade and Military Partnership’, 11 July 2020. This Iran-China cooperation has been going on for several years. Notably, most of the payments between China and Iran, if not all, exclude the US dollar.

[11] For the less well known British escapades in this respect, see the book by Mark Curtis, Secret Affairs: Britain’s Collusion with Radical Islam, 2010.

[12] See here, and for the more official Chinese responses, see here and here.

[13] The Guardian, Germany’s ‘China City’, 1 August 2018.

[14] Comment from Jochen Goller, president and CEO of BMW Group Region China, Asia Times, 6 July 2020.